It has been a couple of days since the ease of restrictions taken to fight COVID-19 in Egypt. Currently, the working hours are longer, many employees are going back to the office, and the curfew was lifted. Moreover, restaurants, cafés, cultural facilities, and religious institutions are now reopened with only 25 percent of their capacity, after being closed for almost 3 months due to the global pandemic.

The new regulations sparked controversy over the safety of the citizens, since COVID-19 cases are still on the rise. Yet, Egypt’s Prime Minister Mostafa Madbouly, explained that the new regulations are motivated by trying to achieve a balance between preventing the spread of the virus and saving the livelihoods of Egyptians. Naturally, the economy faced multiple setbacks since the beginning of the lock-down. But since it’s been a considerable amount of days since reopening, what’s changed in the country’s economy?

Highest Index Score in 4 Months

A man selling tomatoes in Cairo, Egypt

Egypt’s economy started to partially recover, since the implementation of a co-existing plan with the virus. The Egyptian non-oil private sector’s decline rates in both activity and new business slowed considerably compared to last month, reported HIS Markit in a press release on July 6.

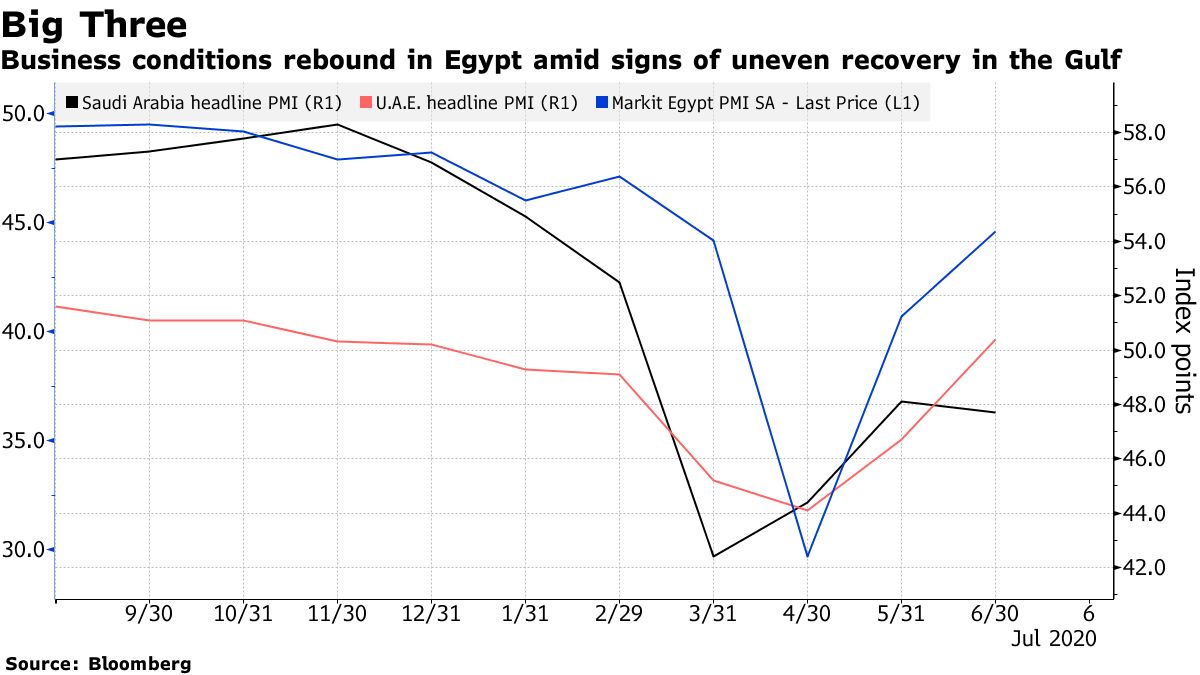

The economic indicator, Purchasing Managers’ Index (PMI) for Egypt, scored its highest rate in 4 months, rising from 40.7 in May to 44.6 in June, getting closer to its index score before COVID-19, which was ranging from 49 to 52.

Although Egypt’s PMI is still below 50, the minimum that separates growth from contraction, the economy is remarkably gaining momentum, compared to April’s PMI, 29.7, which was the lowest rate Egypt reached.

“June’s PMI data gave some promising signs that the Egyptian economy is beginning to stabilize,” David Owen, economist at IHS Markit, said in the report.

A graph comparing the PMI of Egypt, UAE and Saudi Arabia from September 2019 to June 2020

Despite the softer downturn in the private-sector growth, the rate of job loses and laid off employees is still increasing to nearly the highest rate in 4 years, as firms try to reduce costs, according to IHS Markit. Other companies chose to adjust the salaries, and lower the wages, which resulted in the setback of the staff costs for the third month consecutively.

Egypt to Minimize Economic Setbacks by Reviving Tourism

In an attempt to revive the country’s vital tourism sector, Egypt reopened its airports for international flights after 3 months of closure due to COVID-19, early this month. In addition, Egypt’s Tourism Minister, Khaled El-Anany reopened Cairo’s major touristic site, the Egyptian Museum. This goes alongside other entertainment facilities that have reopened including beaches and concerts (so long as open-air).

Egypt’s efforts to rekindle tourism are motivated by the economy, since it is a main source of employment, government revenue, and foreign currency. Without this vital sector, Egypt’s Gross Domestic Product (GDP) would contract and rates of employment would greatly rise.

Hence, the gradual reopening of tourism in Egypt would partially limit the economic setbacks. In fact, a recent study titled “COVID-19 And Tourism” conducted by United Nations Conference on Trade and Development (UNCTAD), assessed the potential consequences of COVID-19 lock-down on the tourism sector in several countries by illustrating 3 possible scenarios based on the severity of international tourism absence.

Change in Skilled Wages (in % changes): 15 most affected countries. Source: UNCTAD

The above graph shows the change in skilled wages in the 3 scenarios: Egypt’s skilled wages change is estimated to be -3% in the moderate scenario, compared to -6 % in the intermediate scenario and -8% in the dramatic one. The moderate scenario entitles the removal of 1/3 of annual inbound tourism, which Egypt is currently seeking to limit the economic setbacks and minimize the changes in wages.

The end of the COVID-19 lockdown and the ease of restrictions were clearly motivated to save Egypt’s economy from collapsing. Business activities, sales and growth have greatly increased in June, yet there still are some downturns, especially in the employment rates.

With a spark of hope in the private sector, changes are still necessary in order to somehow return back to our pre-COVID-19 economy.